Refinancing your student loans can have a significant impact on your debt payoff strategy — including giving you more flexibility and the chance to save money on interest.

But refinancing student loans with bad credit can be challenging.

Here’s why you should still consider it, and what you can do to improve your chances of getting approved for a student loan refinance.

Why you should consider student loan refinancing

Student loan refinancing is the process of combining one or more federal or private student loans into one new loan with a private lender. While refinancing isn’t for everyone, there are some major benefits you may be able to take advantage of if you qualify:

- Savings: Depending on the interest rates on your current loans, refinancing could allow you to get a loan with a lower rate, which would save you money as you pay down your debt and could also lower your monthly payment.

- Flexibility: Private lenders can typically offer repayment terms ranging from five to 20 years, giving you some control over how fast you pay off your debt. A shorter repayment term would increase your monthly payments, but it would also save you money on interest and help you become debt-free faster. On the flip side, a longer repayment term would cost you more in interest, but it could help you reduce your monthly payment to a more manageable level. The important thing is that you get to choose.

- Simplicity: Replacing multiple student loans with just one new loan can simplify your repayment plan. Instead of keeping track of several monthly payments, you just have to make one.

Keep in mind, though, that if you’re refinancing federal student loans, you will lose certain benefits that the U.S. Department of Education provides to borrowers including student loan forgiveness programs, income-driven repayment plans, generous forbearance and deferment options, and more.

Why refinancing student loans with bad credit is hard

The federal student loan program is set up so that borrowers don’t need to undergo a credit check to get approved for a loan. This arrangement works well for college students, who typically haven’t yet had the chance to establish a credit history.

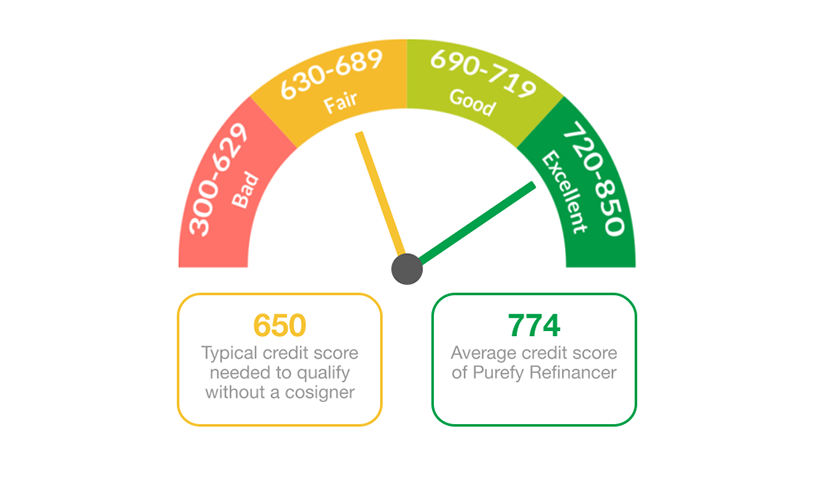

If you’re hoping to refinance, though, you can expect a credit check from a private lender. And, unfortunately, many private lenders require good or excellent credit plus a solid income to qualify. Even then, you may not be eligible for a lender’s lowest interest rate.

As a result, it’s incredibly difficult to get approved for student loan refinancing on your own if you have bad credit. That said, it’s not impossible if you have the right approach.

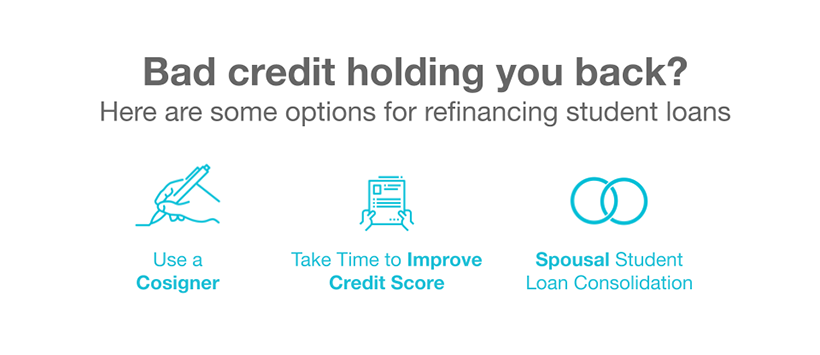

How to refinance student loans with bad credit

If your credit isn’t in great shape, but you still want to try to refinance, your best option is refinancing student loans with a cosigner. This cosigner acts as a co-applicant to effectively guarantee payment to the lender if you can’t keep up with your monthly payments.

If you have a loved one with great credit and income who is willing to cosign, it can improve your chances of getting approved for the loan and offered the lowest rates to help you save significant money.

Also, some lenders offer cosigner release, which allows you to remove your cosigner after you’ve made a certain number of payments and meet the lender’s credit requirements on your own. So if you have bad credit but are in the process of improving your credit score, you may be able to apply for cosigner release down the road.